Understanding Home Equity Loans

May 26, 2025 By Kelly Walker

Homeownership is a significant step for many individuals, and it can provide them with numerous financial benefits. One of these advantages is that you can loan it against the value of your property to pay for large bills. This can be accomplished with a home equity loan. This article will explain what a home equity loan is, the Pros and cons of Home Equity Loan, and the steps required to get one.

What is a Home Equity Loan?

A home equity loan is a form of loan that allows you to borrow money using the value of your property as security. Equity is the gap between the value of a home and the amount still owed on the mortgage.

Pros and Cons of Home Equity Loan

Pros of a Home Equity Loan:

The three main pros of home equity loans are as follows:

Lower Interest Rates

Home equity loans typically have more affordable interest rates than other types of loans. Credit cards and personal loans are included.

Tax Benefits

You can deduct your interest on a home equity loan from your taxes. This can save you money.

Large Loan Amounts

With a home equity loan, you can often borrow more money than with other types of loans.

Cons of a Home Equity Loan:

The three main cons of home equity loans are as follows:

Risk of Losing Your Home

When you take out a loan against the equity in your home, the house itself serves as the collateral. If you are unable to repay the loan, you run the risk of losing your home.

Additional Charges

When you take out a loan against the equity in your house, you may be responsible for paying closing expenses, appraisal fees, and other fees.

Interest Rates Can Change

The interest rate on a home equity loan might fluctuate over time, in contrast to the case with a mortgage with a fixed rate. This can make creating a budget that accounts for your monthly expenses more challenging.

Home Equity Loan Considerations

When considering a loan against the equity in your house, it is essential to consider several technical considerations seriously. When you do this, you can ensure that the decision you make is well-informed and in line with the requirements and aspirations you have for your finances. There are a few things that you need to bear in mind, and they are as follows:

Interest Rates

Although the interest rates on home equity loans are typically lower than those on other loans, shopping around and comparing rates is vital to secure the best possible deal.

Tax Implications

Your interest on a home equity loan might be deducted from your taxes in certain circumstances. Nevertheless, due to recent changes in tax legislation, not all borrowers will be able to benefit from this deduction in the future. Consult with a tax professional if you are interested in learning how the use of your home's equity will influence your tax liability.

Repayment Terms

Most home equity loans have fixed terms for paying them back. The monthly amount you pay won't change as long as you have the loan. Knowing how the loan will be paid back is important, and ensuring you can afford the monthly payments is important.

Alternative Options

A home equity loan is one option for obtaining funds to cover significant financial responsibilities. A personal loan or a line of credit secured by your home's equity are two further options you could consider. It is essential to consider each option's benefits and drawbacks and select the one that caters more closely to your requirements.

Loan Limits

Most loan providers will not allow you to borrow more money than a predetermined proportion of the value of your property. Be sure you know the amount you are eligible to borrow, and don't take out a loan for more money than you can afford to pay back.

Home Equity Loan Requirements

The home equity loan requirements are:

Sufficient Equity

To qualify for a home equity loan, you typically need to have 20% equity in your property.

Good Credit Score

Lenders will examine your credit score when deciding if you can get a home equity loan.

Stable Income

Lenders will also want to see that you have a stable income to repay the loan.

Debt-to-income Ratio

Lenders will look at your debt-to-income ratio, which compares the total amount of debt a person has to the total amount of income that person makes.

How a Home Equity Work?

When you get a home equity loan, the lender will use your house as collateral. Your lender could take your house back and sell it to get the money you owe back. A traditional home equity loan has a set amount of time to repay. The borrower makes fixed payments regularly to cover the debt and the interest. As with any mortgage, the home could be sold to cover the remaining balance if the loan is not paid back.

To get a home equity loan, you must meet certain requirements, such as owning at least 20% of your home, having a good credit score, and having a steady income. You must also pay back your loan every month. Both the principal and the interest will be paid with these payments. It's important to remember that taking out a home equity loan comes with risks. You could lose your home if you didn't make your loan payments. You will also have to pay several different fees.

To Wrap Up

A home equity loan can be a great choice for homeowners. But before getting this kind of loan, it's important to consider the pros and cons carefully. Make sure you know the requirements and that you meet them before applying. If you know what you're doing, a home equity loan could be a good way to get the money you need to reach your financial goals.

Overall Tax Burden by State

See how tax burdens vary across different U.S. states and discover why some are paying more than others. Get a comprehensive look at who pays what with this detailed guide.

May 26, 2025 Rick Novak

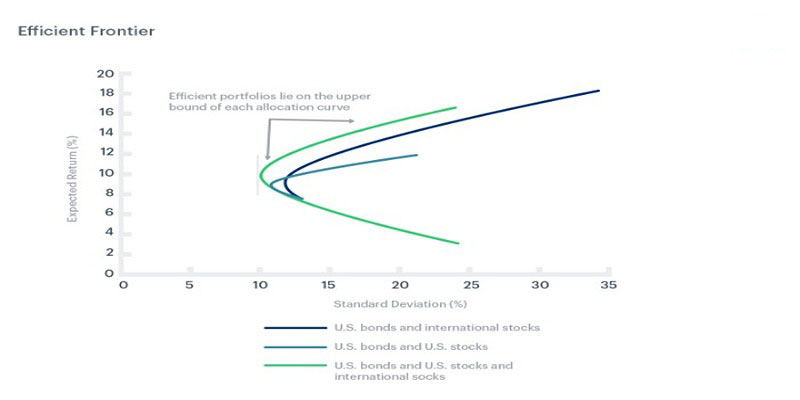

What Is the Efficient Frontier?

Dive into the fundamentals of the efficient frontier and learn how its elements work together for maximum potential gains with minimal risk. Find out all you need to know about it in this helpful blog post!

May 26, 2025 Rick Novak

IPO vs. Private Placement: What's the Difference

IPO is an underwriting by banks which facilitates investments and private placements include investment through pensions, mutual funds, etc.

May 26, 2025 Kelly Walker

Most Prestigious Finance Internships

Learn about the most prestigious finance internships available and get a comprehensive guide on finding the best program for your future career.

May 26, 2025 Kelly Walker

Share Repurchases vs. Redemptions: Pros and Cons

Learn about the pros and cons of share repurchases and redemptions for companies and shareholders. Discover the benefits and drawbacks of each method.

May 26, 2025 Kelly Walker

Best Day Trading Platforms

Find the best day trading platform for you with our comprehensive reviews and analysis. Learn which features set these platforms apart from one another and make an educated decision.

May 26, 2025 Rick Novak