Difference between GAAP and IFRS

May 26, 2025 By Kelly Walker

IFRS (International Financial Reporting Standards) and GAAP (Generally Accepted Accounting Principles) differ in several ways, some of which are as follows:

Inventory management

Companies can value inventory by GAAP using either the FIFO (first-in, first-out) or LIFO (last-in, first-out) procedures. Companies must employ either the FIFO or weighted average cost methodologies by IFRS, which forbids using LIFO.

Treatment of costs associated with research and development

While development costs may be capitalized if certain conditions are met, research costs are generally expensed as they are incurred. According to IFRS, development expenditures are only capitalized if specific requirements are met, and research costs are expensed as they are incurred.

Treatment of goodwill

According to GAAP, goodwill must be evaluated at least once a year for impairment and written down if the carrying value is greater than fair value. According to IFRS, goodwill is likewise evaluated for impairment at least yearly, but the amount of impairment is determined by contrasting the carrying value with the amount that can be recovered.

Revenue recognition

It is based on a four-step process that, according to GAAP, entails identifying the contract, pinpointing the performance commitments, figuring out the transaction price, and allocating the purchase price to the commitments. According to IFRS, revenue recognition is based on a five-step process that entails identifying the contract, pinpointing the performance obligations, figuring out the transaction price, dividing it among the performance obligations, and finally, pinpointing the moment the performance obligations are met.

Leasing accounting

According to GAAP, businesses must categorize leases as operating or finance leases. Since operating leases are also recorded on the balance sheet, the distinction between finance leases and operating leases under IFRS is less important.

These changes can lead to sizable discrepancies in the financial reporting of businesses that use GAAP and those that utilize IFRS. To provide better consistency in financial reporting between the two standards, attempts have been made to converge the two accounting standards. In recent years, some development in this direction has been made.

Advantages of GAAP

Consistency

Consistency is an essential principle of accounting and financial reporting and refers to the use of uniform accounting procedures and practices throughout all financial statements and reporting periods.

Because of consistency, stakeholders can monitor a company's financial performance and spot trends, which makes financial statements comparable across time. For instance, if a company adjusts its accounting rules or practices between reporting periods, comparing the financial statements from the two reporting periods could be difficult.

Consistency is also necessary for making sensible business decisions. If financial statements are inconsistent or not comparable, it may be difficult for investors or other stakeholders to assess a company's financial health and make prudent financial or business decisions.

Compliance

In financial reporting, compliance refers to abiding by laws, regulations, and accounting standards like IFRS (International Financial Reporting Standards) or GAAP (Generally Accepted Accounting Principles).

Compliance is crucial since it fosters accountability and openness while assisting in ensuring the quality and dependability of financial data. A company's reputation may suffer legal and financial repercussions, including fines and litigation if accounting standards or regulations are not followed.

For instance, GAAP compliance in financial reporting is mandated by law for public firms in the United States. If GAAP is not followed, regulatory agencies like the Securities and Exchange Commission (SEC) may take enforcement action, which could harm the company.

Transparency

The disclosure of pertinent financial information in an understandable and transparent way is referred to as transparency, an important tenet of financial reporting.

By giving stakeholders the knowledge they need to make wise decisions, transparency fosters accountability and trust in a company's financial reporting. Due to their obligation to deliver accurate and trustworthy financial information to their shareholders, investors, and other stakeholders, public corporations must be exceptionally transparent.

Better decision-making

Accurate and trustworthy financial reporting can facilitate better decision-making inside a firm. To make informed decisions about business operations, investments, and financing activities, stakeholders rely on financial information. A crucial component of decision-making processes is financial data.

For instance, reliable financial reports can assist management in making defensible choices on resource allocation and investment opportunities. Creditors and investors can also analyze financial data to choose whether to lend money to or invest in a company.

Advantages of IFRS

Global standardization

Because IFRS (International Financial Reporting Standards) provides a uniform framework for financial reporting across many nations and regions, global standardization is a significant advantage of IFRS.

By promoting transparency and accountability in financial reporting, this standardization makes it simpler for businesses to compare financial data across markets and for investors to make wise investment choices.

A collection of accounting standards that are widely accepted and intended to be applied uniformly in many nations and industries are provided by IFRS. By making it simpler for multinational corporations to comply with reporting rules in many markets and cutting down on compliance expenses, this common framework aids in the simplification of financial reporting.

Enhanced financial reporting standards

Improved financial reporting quality is another important benefit of IFRS (International Financial Reporting Standards). Thanks to IFRS's principles-based approach to financial reporting, businesses have more latitude in how they display their financial information.

However, it also necessitates greater judgment and analysis, which can result in more precise and trustworthy financial data.

Enhanced Transparency

One of the main advantages of IFRS (International Financial Reporting Standards) is increased transparency. Businesses are required to disclose all relevant financial information, such as information on their status, performance, and cash flows, by IFRS.

This can improve openness and accountability while improving the company's financial performance for investors. Companies must disclose significant accounting assumptions, judgments, and policies used in generating their financial statements under IFRS.

Purchasing capital

Access to financing is a significant benefit of IFRS. IFRS offers an internationally recognized set of accounting standards, which can make it simpler for businesses to draw in foreign investors and access capital markets in other nations.

Companies can display their financial data in a way that is well-accepted and understood by investors all around the world by adopting IFRS. This could strengthen the financial data's trustworthiness and raise the company's profile on the world capital markets.

Improved reporting

Simplified reporting is another benefit of IFRS. Companies have more freedom in how they present their financial information thanks to IFRS's principles-based approach to financial reporting.

By doing this, businesses may be able to streamline their reporting procedures and lower their financial reporting expenses.

How to choose between IFRS and GAAP?

The decision between GAAP and IFRS is influenced by several variables, including the company's location, industry, regulatory requirements, size, the target audience for the financial statements, and future growth plans.

A corporation must adhere to GAAP if it is headquartered in the United States or conducts business in a nation that does so. Similarly to that, a corporation must adhere to IFRS if its headquarters are in a nation that uses them.

The adoption of IFRS, however, maybe something to think about if a business has operations in several nations or has ambitions to grow internationally in the future.

When choosing which accounting standards to use, a corporation must consider the demands of its stakeholders, including investors, creditors, regulators, and analysts. For instance, if a company's stakeholders are more accustomed to GAAP, it can be advantageous for the business to adhere to GAAP to make the financial statements simpler and more comparable.

The choice of which accounting standards to use should be determined in the end after carefully weighing all of the relevant elements and consulting with accounting experts.

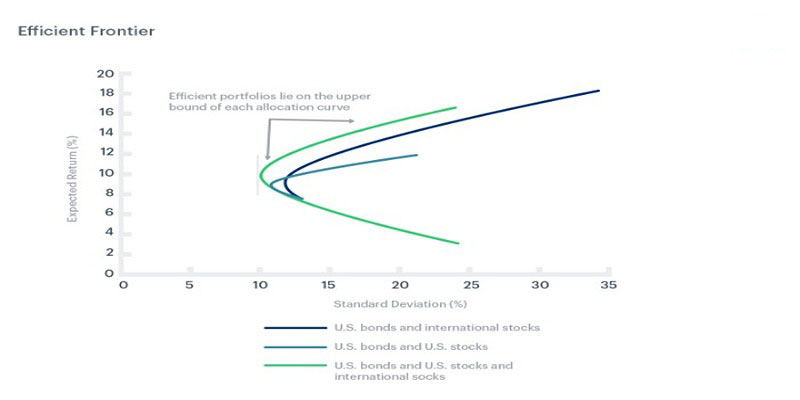

What Is the Efficient Frontier?

Dive into the fundamentals of the efficient frontier and learn how its elements work together for maximum potential gains with minimal risk. Find out all you need to know about it in this helpful blog post!

May 26, 2025 Rick Novak

Difference between GAAP and IFRS

Generally Accepted Accounting Principles (GAAP) and International Financial Reporting rules (IFRS) are two sets of accounting rules that businesses use to develop and display their financial accounts. While IFRS is utilized in many other nations throughout the world, GAAP is a set of accounting standards that are predominantly employed in the United States. The geographical scope is the main distinction between IFRS and GAAP.

May 26, 2025 Kelly Walker

Single-Use Credit Cards: A Detailed Overview

This article will discuss how single-use credit cards work and can be beneficial and what are the drawbacks of these cards!

May 26, 2025 Kelly Walker

How Is Cashback Profitable for Credit Card Companies?

Get insights into how credit card companies benefit from cashback programs, plus some examples that demonstrate the profitability of this type of reward program.

May 26, 2025 Kelly Walker

Corporate Tax Rates Around the World: From the Highest to the Lowest

Here are the nations that have the most favorable business tax environments and which impose the highest tax burdens on corporations. Whether you're an entrepreneur looking to minimize your tax liabilities or simply curious about global tax policies, this article provides valuable insights into the world of corporate taxation.

May 26, 2025 Kelly Walker

Most Prestigious Finance Internships

Learn about the most prestigious finance internships available and get a comprehensive guide on finding the best program for your future career.

May 26, 2025 Kelly Walker